The age of information in which we live is amazing. Answers, opinions and misinformation are everywhere. Renewable energy, specifically photovoltaic solar (PV solar), is no different. I’ve discovered more and more social media posts as well as opinion based articles from specialized news outlets that are not fact based but categorically false. Ironically, they are on both sides of the pro and anti renewable spectrum. Therefore, I believe it’s necessary to post some basic questions and answers based on my experience in the industry. If you are seeking genuine real world industry answers these would be mine.

1. What is the business case for commercial PV solar?

Answer: Commercial PV solar is a long term operating cost control and energy risk management asset for a business. It reduces purchased kWh, hedges against future utility rate increases, supports sustainability goals, and creates an owned energy asset with a 25+ year useful life. Financial incentives and depreciation improve the economics of the investment. Each business case is different and, in some cases, it may not work for an organization.

2. What are the financial benefits of installing solar for a commercial business?

Answer: The main financial benefits are reduced utility energy purchases, potential federal tax credit value (currently sunsetting), depreciation benefits, utility or state incentives (where available), and long term savings by producing electricity onsite. The value depends on load profile, utility rate plan structure, installation cost, tax appetite, incentive availability and financing. It’s not always a good fit for every business. It depends on your situation.

3. What are the non financial benefits of commercial solar?

Answer: Non financial benefits include sustainability leadership, lower emissions (important when you are in an emission control district), customer and stakeholder goodwill, energy independence, and the ability to prepare for future batteries, EV charging, or an onsite microgrid for resilience. Solar can also help meet corporate Environmental Social Governance, supplier, or public sector CO2 energy reduction goals if they have been set or mandated.

4. How does solar reduce utility electricity costs?

Answer: Solar reduces utility costs by generating electricity onsite that offsets kWh otherwise purchased from the utility. The savings are strongest when solar production lines up with daytime business loads and when exported energy is credited at a favorable rate. When paired with batteries it can further reduce operating costs for utility KW demand fees. Depending on the utility rate plan structure versus the cost of the investment determines if the case for investment should be made.

5. How does solar reduce exposure to future utility rate increases?

Answer: Each kWh produced by the solar system is a kWh the business does not buy from the utility, so the owner is partially insulated from future energy rate escalation. This hedge is valuable because the solar system cost is largely fixed upfront while utility rates and riders can change over time.

6. What types of businesses benefit most from solar?

Answer: Businesses with high daytime electrical consumption, large roofs or land, long term site control, and the ability to use tax benefits usually benefit most. In some situations, the value of solar shade structures can drive investment i.e. solar covered car parking, diminished water evaporation, agri photovoltaics, etc. Examples include manufacturing, warehouses, cold storage, schools, public facilities, tribal facilities, agricultural operations, and fleet depots.

7. What industries are adopting commercial solar?

Answer: Common adopters include manufacturing, logistics, agriculture, education, healthcare, municipalities, tribal governments, retail centers, water and wastewater facilities, and fleet operators. Adoption is strongest where utility electricity costs are high, site control is long term, and the organization values energy cost predictability, independence and resilience. The biggest driver of adoption is the leadership in an organization. It’s generally a decision of economics, independence, resilience or carbon offset/ reduction.

8. What are the risks of not installing solar?

Answer: Risks include continued exposure to utility rate increases, missed incentive windows, inability to control a portion of energy costs, and falling behind customer or stakeholder sustainability expectations. Delaying may also reduce access to tax credits, rebates, grants, or favorable interconnection capacity when these are available. In some cases, the risk is minimal, this is especially true if renewables are not an achievable investment whether its due to space, energy load or a financial ROI period based on an organization’s acceptable standards. Each business case is different.

9. How does solar support sustainability or ESG goals?

Answer: Solar supports sustainability goals by reducing grid electricity purchases and the emissions associated with operations. It also creates measurable data for Environmental Social Governance reporting, including annual kWh production, estimated avoided emissions, and progress toward renewable energy targets.

10. How does solar improve energy independence?

Answer: Solar improves energy independence by allowing a facility to produce part of its electricity onsite. Solar alone generally does not provide backup power during a grid outage unless it is paired with batteries, a generator, transfer equipment, and controls that allow safe islanded operation. Grid connected solar systems (in most cases they are all grid connected) will shut down when there is a utility power grid loss. This is to ensure the solar system does not back feed into the grid. It ensures safety for line workers and allows the utility to more easily address the issue causing the outage. If you want electricity from your solar system during an outage a battery is necessary regardless if it is the day or night.

11. How is a commercial solar system sized?

Answer: A commercial solar system is sized by reviewing annual and interval load data, available roof/land area, utility rate structure, interconnection limits, export rules, budget, and owner goals. The best size is usually the system that maximizes useful onsite energy value rather than simply maximizing nameplate capacity. Each situation is unique to itself and all of these factors need to be considered to identify if it is appropriate for a business to adopt or not.

12. How much roof or land area is needed for solar?

Answer: Area depends on module wattage, racking type, access pathways, setbacks, tilt, row spacing, and site constraints. The best answer is identify the overall site load can be offset with the available space and is justified by the investment.

13. What is the difference between kWdc and kWac?

Answer: kWdc is the direct current nameplate capacity of the PV modules; kWac is the alternating current output capacity of the inverters. The DC size is usually larger than the AC size because modules rarely operate at nameplate output continuously. This is pretty technical and, in most cases, not important to know for a business owner to fully understand. It’s generally conversation for the contractor, engineer and utility but sometimes people ask.

14. What is the typical DC/AC ratio for commercial solar?

Answer: The DC/AC ratio compares PV module capacity to inverter capacity. Commercial and utility systems often use ratios around 1.2 to 1.4, but the optimal ratio depends on climate, clipping tolerance, inverter cost, interconnection limits, and production goals. It’s another technical conversation among designers and engineers that isn’t relevant to most decision makers but its good to understand what it means if it ever comes up in conversation.

15. What is the expected annual production from a commercial PV system?

Answer: Expected annual production is estimated with solar modeling software using weather data, module orientation, tilt, shading, losses, inverter capacity, soiling, degradation, and availability. Results are commonly reported as kWh/year and specific yield in kWh/kWdc. The benefit of PV solar is predictability over time. Cloudy or rainy days have an impact on production so does shade or dust build up as well as PV module degradation. All of these need to be considered in the equation for output. In general terms solar production is a long term game and if your self producing then you’re going to see benefit. Solar systems are like any other piece of equipment they diminish in output over time but system maintenance ensures operability and production over time

16. How does shading affect PV output?

Answer: It absolutely affects output negatively. Trimming trees or vegetation around systems is a must. Designing a system to mitigate or avoid shading is the standard of a good design.

17. What is the difference between rooftop, carport, and ground-mounted solar?

Answer: Apart from the obvious answers on the structure type if you have a choice then the lowest cost option in order are ground mount, then rooftop and finally carport (shade structure). However, there are benefits to each and depending on budget, goals and intention for revenue (fee to park under shade structure) then the approach for the business for adoption may be different.

18. How does single axis tracking compare to fixed tilt solar?

Answer: In terms of PV solar output trackers are much more advantageous. Fix tilt ground mounts are becoming less and less the choice for install in large PV installations. Small scale installations will most likely be fixed tilt. The upside to fixed tilt is that O&M costs are much less since trackers have moving parts that wear out or fail. However, the cost benefit analysis of the project opportunity always includes an O&M factor.

19. What is the useful life of a PV system?

Answer: Commercial PV systems are commonly planned for 25 to 35 years of operation. (I know of and witnessed systems being online producing past +20 years in the field in Arizona) Modules degrade gradually, inverters can fail in time, and some balance of system components (wiring, connections, etc.) may require replacement during the life of the system. In general terms, as long has the installer has best practices in place for design and installation the system will have minimal failures. Maintenance is required for manufacture warranties, longevity and maximum output. There is a difference between PV solar module manufacturers’ quality of equipment and the same is true with inverters. Working with a professional that has years of experience is valuable when choosing good equipment.

20. How much maintenance does a commercial solar system require?

Answer: A regular schedule is a must. Our service agreements layout a two year site visit schedule to inspect, check tolerances, clean equipment etc. Modern systems having online monitoring portals that provide detailed production output data that allows you to keep an eye on the system. However, you still need to have technicians do site visits to be proactive on maintenance. They use the monitoring data to pinpoint issues on the system which helps reduce time in the field.

21. What is the current cost per watt for commercial solar?

Answer: Installed cost depends on system size, mounting type, equipment selection, labor, interconnection, civil work, permitting, utility upgrades, and tariffs. Pricing changes especially when we see bottle necks in supply, tariffs or incentives being applied or sunsetting away. In general terms the overall cost of installed renewable energy generation systems continues to decrease. Renewable energy technologies continue to improve in output, availability, technology, lean manufacturing, global adoption and this has benefited the investor. Each situation is different but in general if the cost to install and operate a PV solar system was not feasible or financially advantageous then there wouldn’t be a growing global industry built around the technology.

22. What is the installed cost of rooftop solar versus ground mount solar?

Answer: It depends on a number of factors that need to be included in a cost analysis to determine the answer. It constantly changes like every other construction project you evaluate as an investment. However, in general terms if you have space a ground mount system typically costs less.

23. What is the payback period for commercial solar?

Answer: Great question, the answer depends on your situation. A proper ROI analysis include utility rates, degradation, O&M, tax benefits, financing, replacement costs, and escalation assumptions. In general terms, we have answers that support an installation type specific to a rate plan which is specific to a utility. Its not too hard for us to provide an answer but we always look at opportunities on case by case basis.

24. What is the levelized cost of energy for solar?

Answer: LCOE is the lifetime cost of producing electricity divided by lifetime energy production, usually expressed in $/kWh. It is useful for comparing solar to utility energy costs, but it does not fully capture demand charges, resilience, tax timing, or financing structure. Again, it’s specific to construction costs of the project versus output expectancy of the system.

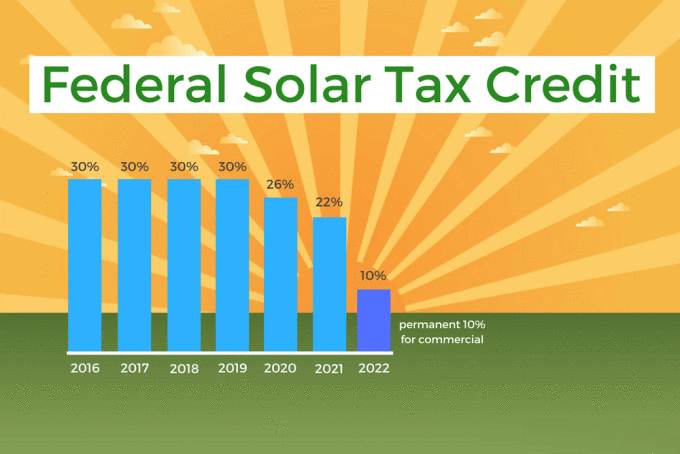

25. How do tax credits affect solar ROI?

Answer: Tax credits always improve ROI. The Inflation Reduction Act was full of tax credits created to further incentivize renewable adoption in the US. The One Big Beautiful bill deconstructed those incentives. The result is that adoption will slow versus its previous potential with incentives that would have been in place. However, the industry must adapt to become more efficient, cost effective and creative to continue to grow. The truth is that governments always incentivize energy production. Fossil fuels are much older form of technology that is more firmly established with a +100-year head start and absolute global adoption. The future is a mix of both renewable and non renewable energy generation to power our needs for energy.

26. How do depreciation benefits affect solar ROI?

Answer: It depends on which accounting practice you use in your calculation. Commercial solar, storage, and charging equipment may qualify for depreciation benefits depending on ownership and tax rules. In PV solar there is a 100% Bonus Deprecation that can be applied to the asset. The value calculation depends on basis, bonus depreciation availability, MACRS classification, taxable income, and tax advisor review of the business financial situation to correctly calculate this.

27. How does utility rate structure affect solar savings?

Answer: Each rate plan is different which makes the opportunity for PV solar different for a system owner. To make PV solar advantageous versus the utility (which may be delivering PV solar generated energy to your meter) the overall cost of the electricity you generate on your system must be less than the current cost you pay to purchase it from a utility. It’s about the lowest cost of energy today at the point in time of installation of the system. In time, over the life of the system the cost to produce energy should continue to be less and increase the cost savings as utility rates typically increase. Utilities sometimes change their rate structures which changes the value proposition of self generation of PV solar. In general terms, utility kWh rates don’t decrease but it is possible. Anything is possible. It’s not likely.

28. How do demand charges affect solar economics?

Answer: Solar may reduce demand charges if its output coincides with the customer monthly peak, but the reduction is not guaranteed. Batteries are required to significantly reduce demand charges. If loads are constant and predictable then load management is predictable because they can discharge during peak intervals or the most cost effective time frame.

29. What is the expected O&M cost for commercial solar?

Answer: Maintenance includes annual telecom subscription fees (monitoring), visual inspections, vegetation control, inverter service, torque checks, thermal scans, cleaning where justified, and corrective maintenance. A sound O&M plan properly accounts for these and should include a percentage cost increase over time that accounts for inflation.

30. How does inflation affect long term solar value?

Answer: Inflation in PV solar systems needs to be accounted for like inflation in any other business cost calculation. Typically, its going to be applied to two categories in the calculation for value proposition. First, the cost of assumed utility electricity over time and the cost to maintain the system over time. Historically, we’ve seen the cost of power electronics and PV modules decrease so if there is equipment that needs to be replaced outside of a MFG warranty the historical trend has worked in favor of the asset owner.

31. Is there a cost associated with project evaluation?

Answer: In general terms no but it depends on the project and the level of analysis being performed. If environmental or land studies need to be done, then yes. However, we typically are able to evaluate most projects at no cost and provide answers to clients to help them understand their opportunity.